There has been a recent debate in the newspapers that the accumulation of FX Reserves over the last three years have been achieved through external borrowings. This is a classic example of viewing a glass of water as “half full or half empty”. One needs to appreciate that money is fungible and the conclusive argument can’t be made for a rational mind that the money raised can merely be used for one specific purpose. There’re surely various permutations and combinations that could be worked out to assess the actual utilization of the funding raised from the external sources by Pakistan. The superfluous view of the situation may lead one to jump to the incorrect conclusion that the FX Reserves are built through borrowings. However, a deeper and thorough analysis will reflect on things very differently – glass half full – and arrive at the right conclusion:

Pakistan’s FX Reserves have been built based on real FX flows; not through external borrowings.

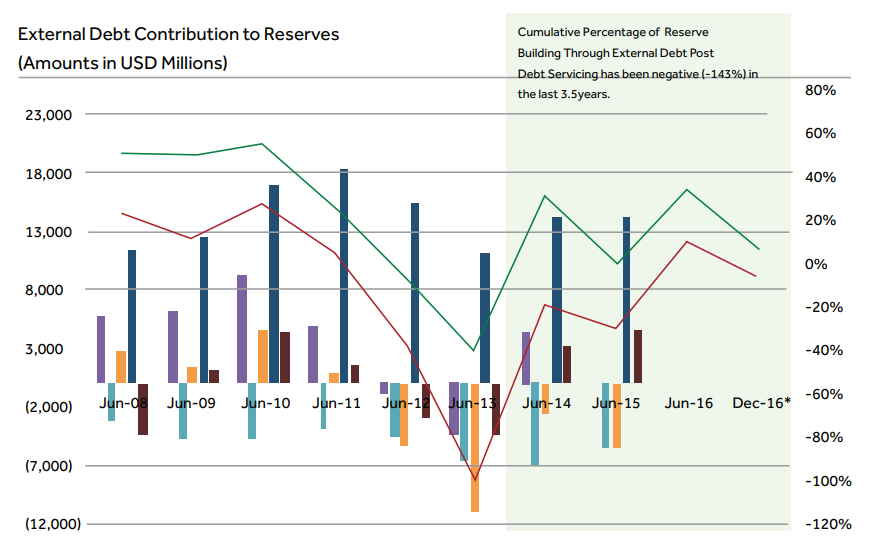

An unbiased assessment of the situation will lead to the fact that if the scheduled maturities of the past FX debt are taken into account then the net addition of marginal debt acquired during the period into FX Reserves is actually “negative” by a large number/ margin of around 143%, i.e., the incremental FX flows were actually used for paying off debt acquired before 2013.

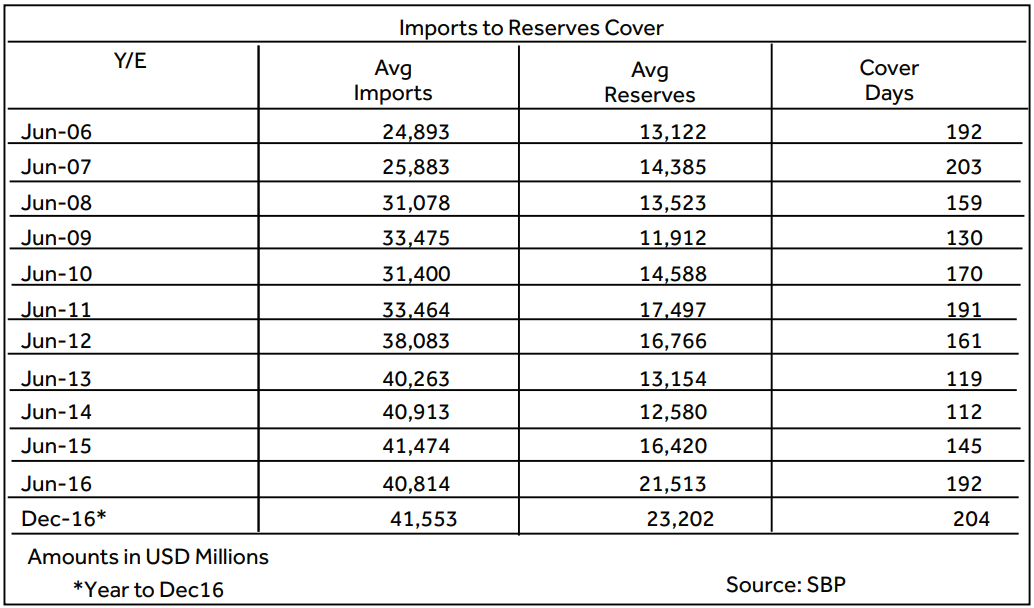

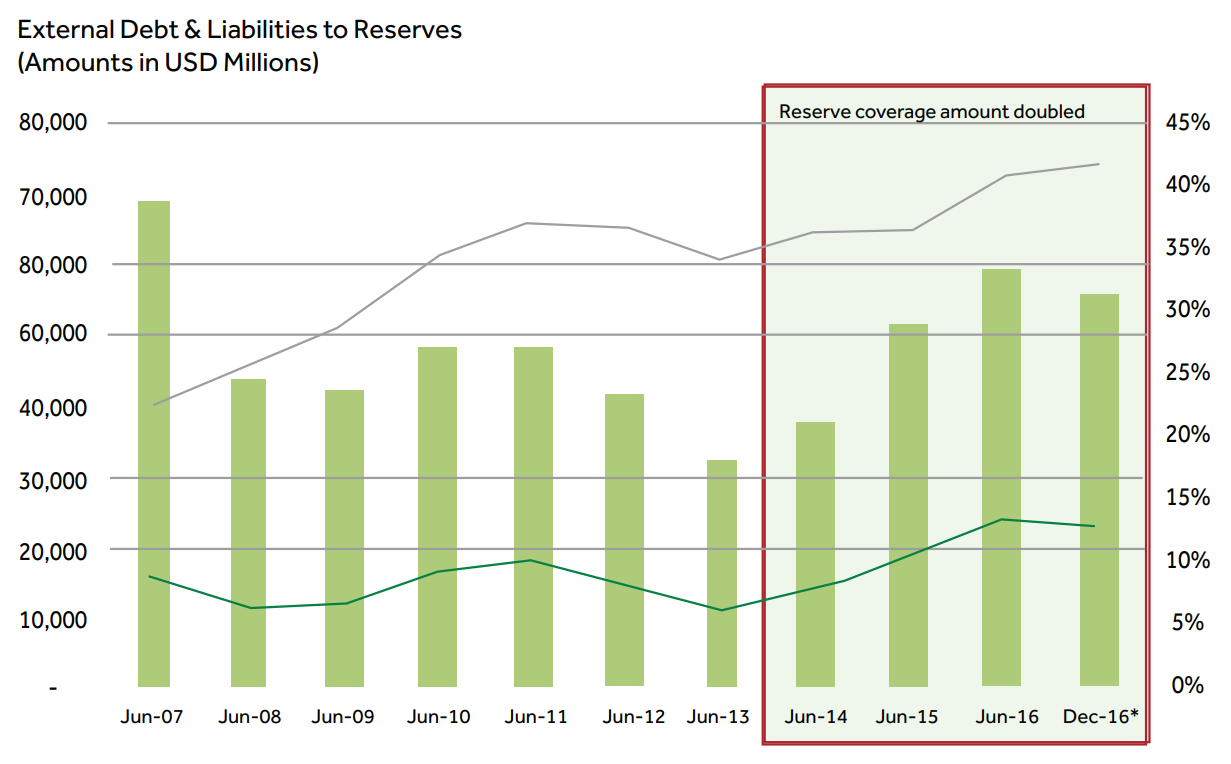

Additionally, let’s also see where does things stand without accounting for the scheduled FX obligations/ debt maturities. Import coverage has been enhanced from 119 days to 204 days. This is by no mean a small achievement. Similar is the situation on the coverage of external debt and liabilities which doubled in the last three years. This is also the reason why our currency remained strong and our external account remained comfortable and defeats the academic thesis that the currency is over-valued.

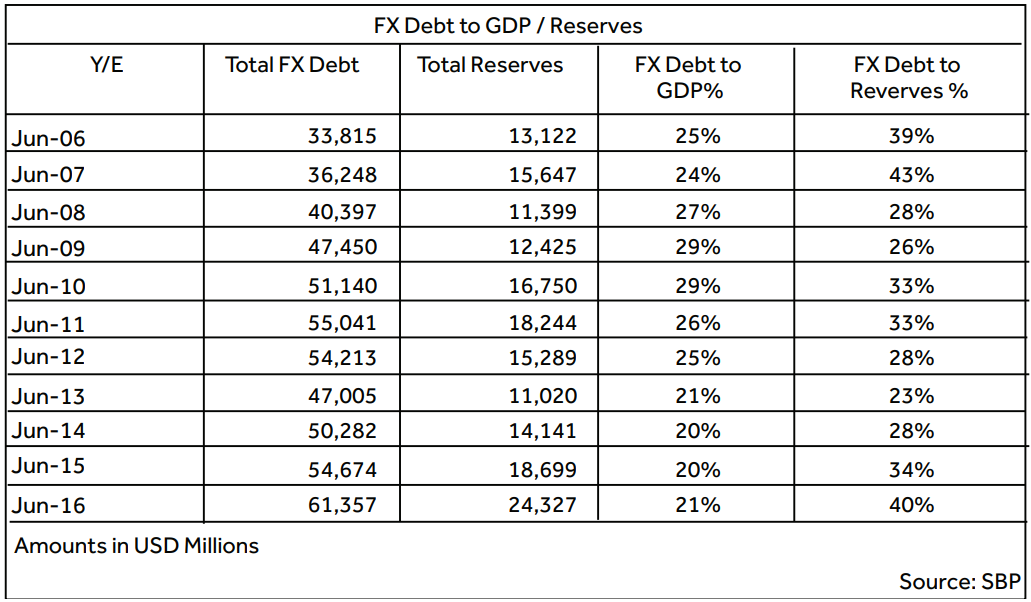

Furthermore, please note that the external borrowings as the percentage of total borrowings have actually come down over a period of time and the decline was much sharper since 2013. Comparing External Debt and Liabilities to FX Reserves show that the FX Reserves coverage has almost doubled in the last three and a half years.

After looking at this data and assessment, the argument that FX Reserves are built based on external borrowings doesn’t hold waters whichever way the data is cut. This data also defeats the notion that Pakistan is sort of stuck in a debt trap, as the data proves that the previously acquired debt is being settled through the reserves and the external flows other than the fresh debt.

Previous

Next